Services

Compliance Monitoring

File Reviews

File Pre-Approvals

State/Investor Audit Preparation

Site Inspections

Training

Overview

Introduction to LIHTC Compliance

Keeping In Compliance: LIHTC Tenant Files

Personalized LIHTC Training

State Monitoring

Overview

American Samoa

California

Connecticut

Delaware

Hawaii

Massachusetts

West Virginia

Forms

About Us

Our Story

Our Team

News

Contact

eLearning Portal

Client Docs

Select Page

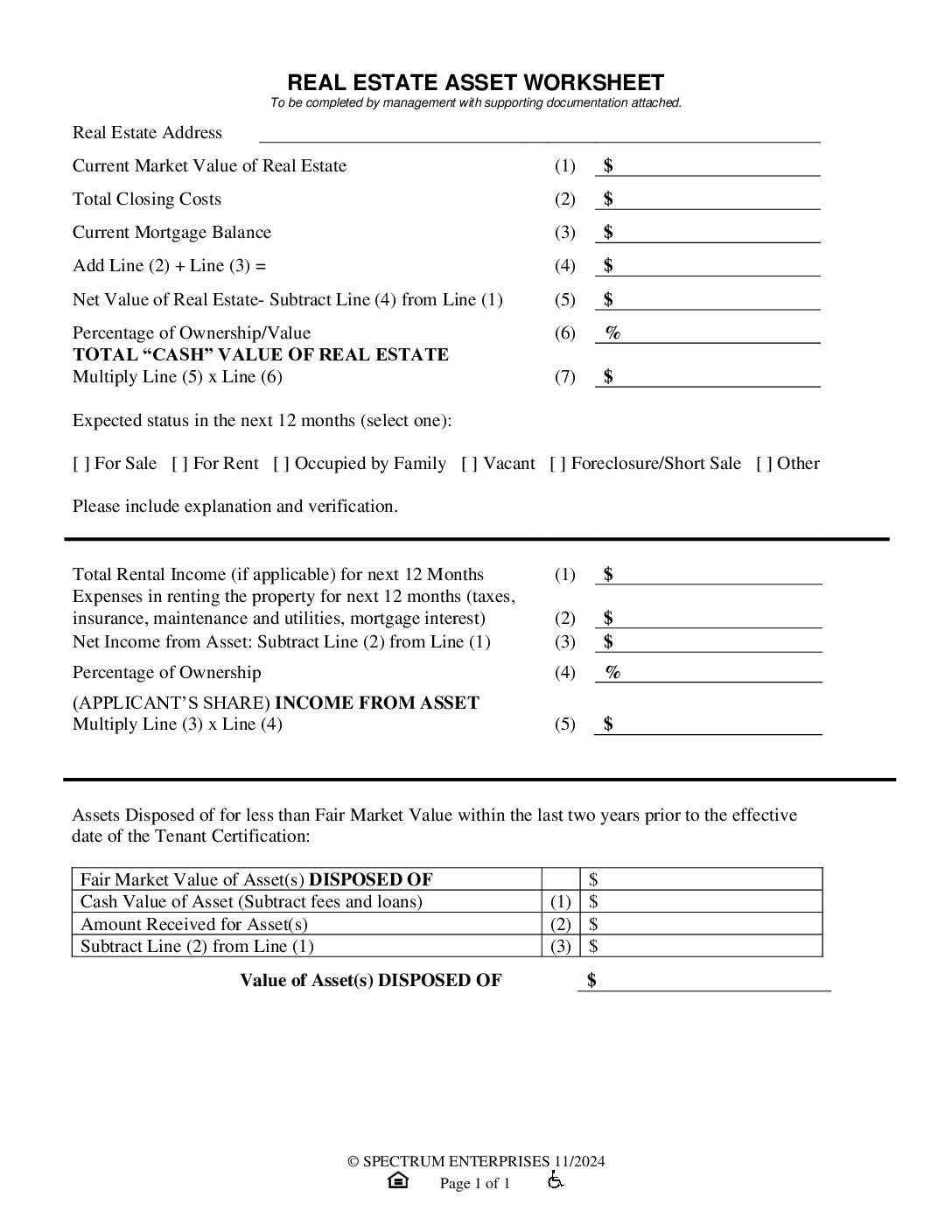

Real Estate Asset Worksheet

Jun 25, 2021

Used by manager to show real estate calculations